PANAMA: Double Tax Treaties

Panama is known for its tax-friendly and dynamic corporate environment attracting investors and entrepreneurs from other countries and contributing to economic stability.

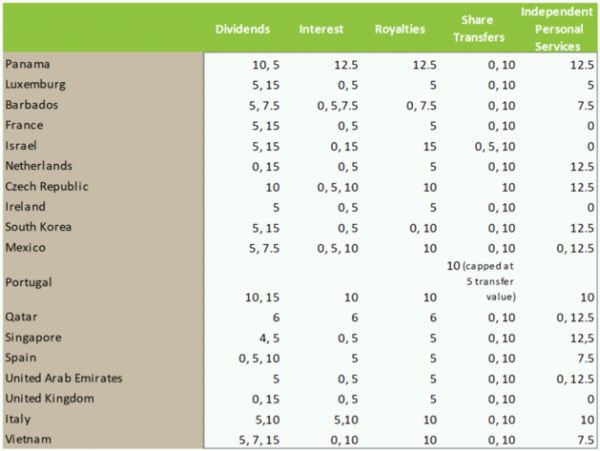

To date, Panama has entered into 17 DTAs in force with Mexico, Barbados, Qatar, Spain, Luxembourg, Netherlands, Singapore, France, South Korea, Portugal, Ireland, Czech Republic, Unit Arab Emirates, United Kingdom, Israel, Italy and Vietnam; that basically recognize and reduce tax rates or the non-application of withholding taxes for certain type of income, such as royalties, interest, dividend and services.

Under Panama's domestic law the following withholding tax rules apply:

- Dividends are subject to a 10% dividend tax when paid out of domestic profits; the rate drops to 5% when the dividends are paid out of foreign-source or export profits, or out of certain income (e.g. interest from government bonds and capital gains derived from the sale of such bonds and interest on bank deposits)

- Interest is subject to a 12.5% withholding tax.

- Royalties are subject to a 12.5% withholding tax.

- Capital Gains on the sale or transfer of capital or securities economically invested in Panama, either directly or indirectly, are subject to a fixed rate of tax of 10%. Nonetheless, the buyer will always be required to withhold from payment and remit to Tax Authorities an amount equal to 5% on the aggregate proceeds of the sale, as an advance payment of the capital gain tax. The transfer of other assets is subject to a 10% capital gain tax.

- Independent personal services. Withholding tax will apply if payments relate to services rendered within or outside Panama regarding a taxable income-generating activity. Withholding tax rate is of 12.5% for companies, and when rendered by an individual applicable tax rates will be those related to natural persons on 50% of the amount invoiced.

Who could benefit from Double Tax Treaties?

Up to this date, there are 177 multinational corporations operating from Panama. Branches of foreign corporations established in Panama declare their income in the country and have executives or employees who generate income in Panama and are not permanent residents.

Regarding the payment of dividends, interests, and bonuses, for example, a branch in Panama that pays dividends to their shareholders outside of Panama must deduct 5%; however, if the shareholders are residents in some of the countries Panama has a treaty with, the branch or the shareholder, according to the treaty guidelines, could demand its government tax credit on the tax withheld by Panama, thus avoiding the double tax imposition.

Those foreign corporations looking into establishing in Panama as branches of companies abroad that generate operations and income and have the required notices of operations may benefit from these treaties.

The Rules

Under Panama's domestic law the following withholding tax rules apply:

- Dividends are subject to a 10% dividend tax when paid out of domestic profits; the rate drops to 5% when the dividends are paid out of foreign-source or export profits, or out of certain income (e.g. interest from government bonds and capital gains derived from the sale of such bonds and interest on bank deposits)

- Interest is subject to a 12.5% withholding tax.

- Royalties are subject to a 12.5% withholding tax.

- Capital Gains on the sale or transfer of capital or securities economically invested in Panama, either directly or indirectly, are subject to a fixed rate of tax of 10%. Nonetheless, the buyer will always be required to withhold from payment and remit to Tax Authorities an amount equal to 5% on the aggregate proceeds of the sale, as an advance payment of the capital gain tax. The transfer of other assets is subject to a 10% capital gain tax.

- Independent personal services. Withholding tax will apply, if payments relate to services rendered within or outside Panama regarding a taxable income-generating activity. Withholding tax rate is of 12.5% for companies, and when rendered by an individual, applicable tax rates will be those related to natural persons on 50% of the amount invoiced.

The following table show a comparison of benefits under Panama's domestic law as compared to the treatment under the tax treaties that are currently in force:

* Applicable tax rate may differ from treaty rates (e.g. lower rate/exemption under domestic law). Specific conditions will have to be observed to benefit of a reduce rate or the non-application of withholding taxes.

Should you have any questions or seek any assistance, please contact us.

Pardini & Asociados